ScholarMatic: Explanation & Answer

Your ready answer from a verified tutor is just a click away for as little as $14.99

Click Order Now to get 100% Original Answer Customized to your instructions!

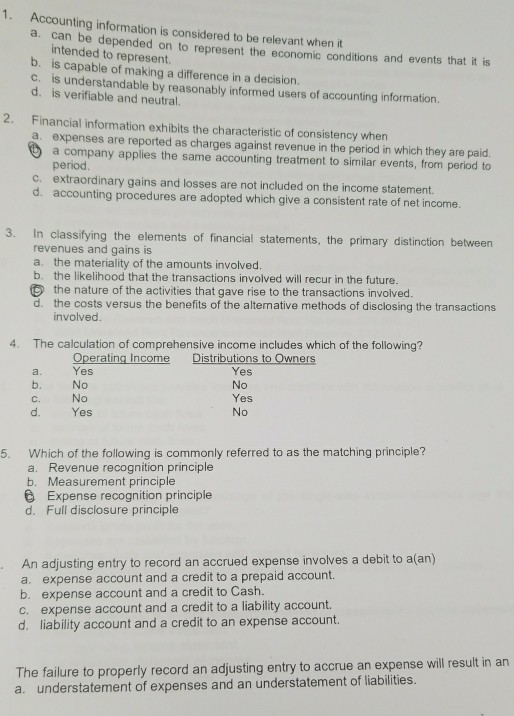

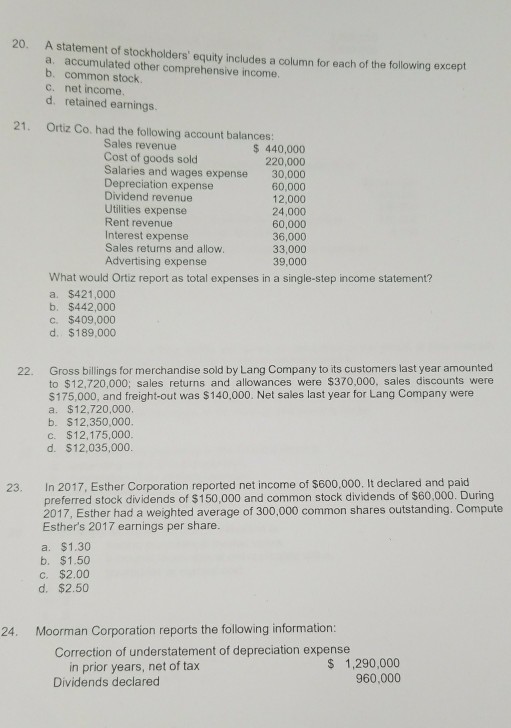

Show transcribed image text 1. Accounting information is considered to be relevant when it a. can b e depended on to represent the economic conditions and events that it is intended to represent. b. is capable of making a difference in a decision. C. is understandable by reasonably informed users of accounting information. d. is verifiable and neutral. 2. Financial information exhibits the characteristic of consistency when a. expenses are reported as charges against revenue in the period in which they are paid. 5 a company applies the same accounting treatment to similar events, from period to period c. extraordinary gains and losses are not included on the income statement. d. accounting procedures are adopted which give a consistent rate of net income. In classifying the elements of financial statements, the primary distinction between revenues and gains is a、 the materiality of the amounts involved b. the likelihood that the transactions involved will recur in the future. © the nature of the activities that gave rise to the transactions involved. d、 the costs versus the benefits of the alternative methods of disclosing the transactions 3. involved. The calculation of comprehensive income includes which of the following? a No 4. Distributions to Owners Operating Income Yes Yes No Yes No C. d. Yes Which of the following is commonly referred to as the matching principle? a. Revenue recognition principle b. Measurement principle 5. Expense recognition principle d. Full disclosure principle An adjusting entry to record an accrued expense involves a debit to a(an) a. expense account and a credit to a prepaid account. b. expense account and a credit to Cash. c. expense account and a credit to a liability account. d. lilability account and a credit to an expense account. The failure to properly record an adjusting entry to accrue an expense will result in an a. understatement of expenses and an understatement of liabilities

1. Accounting information is considered to be relevant when it a. can b e depended on to represent the economic conditions and events that it is intended to represent. b. is capable of making a difference in a decision. C. is understandable by reasonably informed users of accounting information. d. is verifiable and neutral. 2. Financial information exhibits the characteristic of consistency when a. expenses are reported as charges against revenue in the period in which they are paid. 5 a company applies the same accounting treatment to similar events, from period to period c. extraordinary gains and losses are not included on the income statement. d. accounting procedures are adopted which give a consistent rate of net income. In classifying the elements of financial statements, the primary distinction between revenues and gains is a、 the materiality of the amounts involved b. the likelihood that the transactions involved will recur in the future. © the nature of the activities that gave rise to the transactions involved. d、 the costs versus the benefits of the alternative methods of disclosing the transactions 3. involved. The calculation of comprehensive income includes which of the following? a No 4. Distributions to Owners Operating Income Yes Yes No Yes No C. d. Yes Which of the following is commonly referred to as the matching principle? a. Revenue recognition principle b. Measurement principle 5. Expense recognition principle d. Full disclosure principle An adjusting entry to record an accrued expense involves a debit to a(an) a. expense account and a credit to a prepaid account. b. expense account and a credit to Cash. c. expense account and a credit to a liability account. d. lilability account and a credit to an expense account. The failure to properly record an adjusting entry to accrue an expense will result in an a. understatement of expenses and an understatement of liabilities

ScholarMatic: Explanation & Answer

Your ready answer from a verified tutor is just a click away for as little as $14.99

Click Order Now to get 100% Original Answer Customized to your instructions!